Protecting Your Legacy: Understanding the Different Types of Life Insurance

Life is filled with responsibilities, dreams, and the desire to create a meaningful future for the people we love. Whether you're building wealth, raising a family, running a business, or planning for retirement, one question eventually becomes unavoidable:

What happens to the people and goals you care about if you're no longer here?

While no one enjoys thinking about worst-case scenarios, preparing for the unexpected is one of the most powerful acts of care and responsibility a person can make. That is where Life Insurance becomes more than a financial product—it becomes a strategy for protecting the future.

Many people think Life Insurance simply provides a payout after death. In reality, modern policies can serve multiple purposes: income replacement, wealth transfer, debt protection, estate planning, business continuity, and even long-term financial growth.

Yet despite its importance, many people remain confused about the different options available. Terms like term life, whole life, universal life, and cash value can quickly become overwhelming.

Understanding the different types of Life Insurance empowers you to make informed decisions—not based on fear, but based on purpose.

Let's explore the major categories of Life Insurance, how they work, and how each option may fit into your long-term financial legacy.

Why Life Insurance Matters Beyond Death Benefits

When people hear Life Insurance, they often focus only on one outcome: a payout after someone passes away.

But legacy protection goes much deeper.

At its core, Life Insurance helps preserve stability when life becomes uncertain.

A policy can help your family:

Replace lost income

Pay off debts

Cover mortgage obligations

Fund children's education

Protect retirement goals

Preserve family assets

Pay estate taxes

Support business continuity

Without financial preparation, surviving family members often face emotional stress alongside financial hardship.

The goal isn't simply wealth.

The goal is protection.

Understanding the Two Main Categories of Life Insurance

Most Life Insurance policies fall into two broad categories:

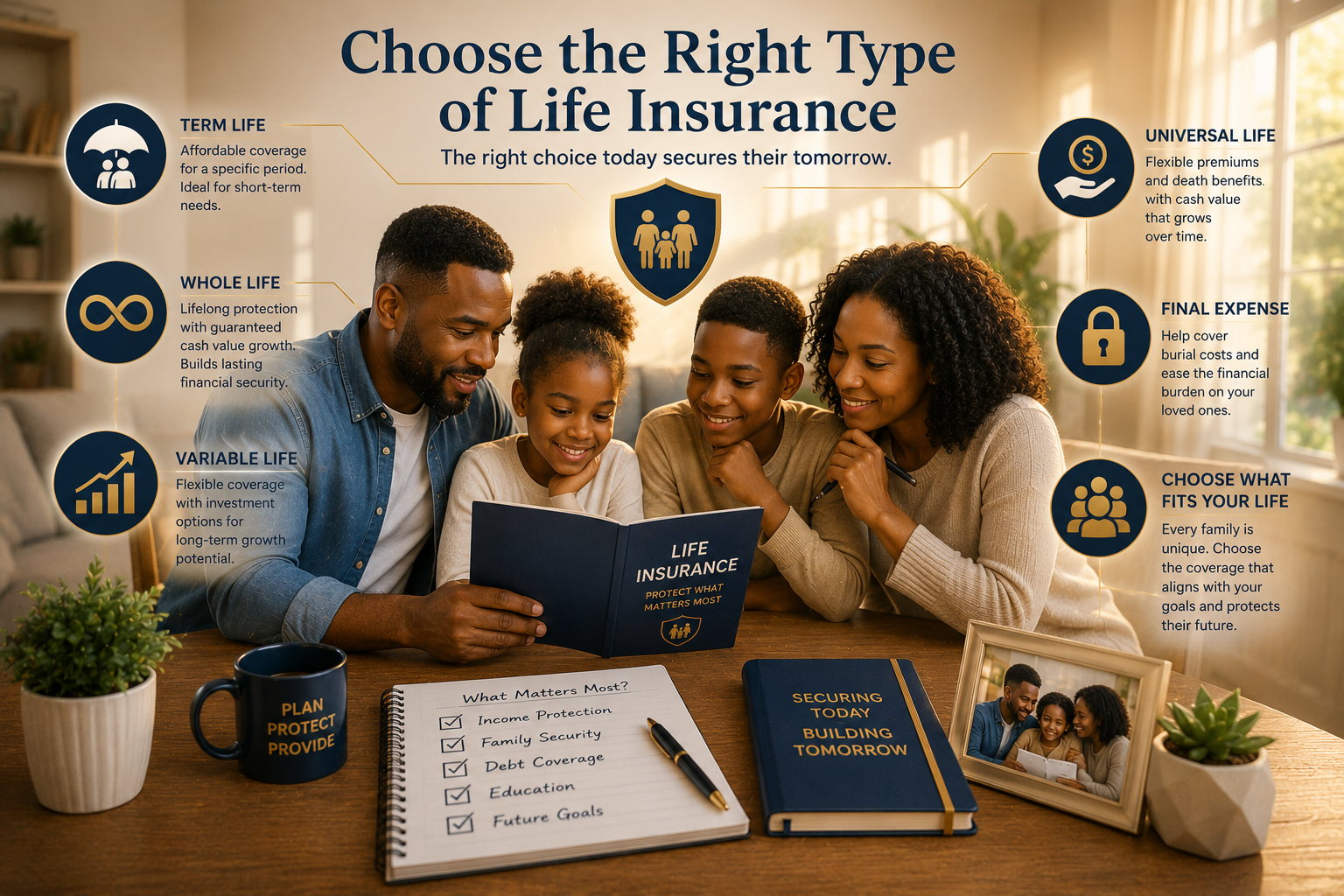

1. Term Life Insurance

Coverage for a specific period.

2. Permanent Life Insurance

Coverage designed to last your entire life.

Within these categories are several variations with unique features and purposes.

Understanding the distinction is the foundation of making smart decisions.

Term Life Insurance

Term Life Insurance provides coverage for a predetermined number of years.

Common terms include:

10 years

15 years

20 years

30 years

If the insured person passes away during the policy term, beneficiaries receive the death benefit.

If the term ends and coverage expires, no payout occurs unless the policy is renewed or converted.

Advantages of Term Life Insurance

Many financial professionals recommend Term Life Insurance as a starting point because it offers:

Affordability

Premiums are typically lower than permanent policies.

Simplicity

Coverage is straightforward and easy to understand.

Larger coverage amounts

People often obtain substantial protection at lower costs.

Flexibility

Useful during specific financial stages.

Examples include:

Raising children

Paying off a mortgage

Covering college expenses

Replacing working income

Potential Drawbacks of Term Life Insurance

Although valuable, term coverage has limitations:

Coverage eventually ends

Premiums may rise if renewed

No cash accumulation

Benefits disappear if the policy expires

For some people, temporary protection aligns perfectly with financial goals.

For others, permanent coverage may offer greater long-term value.

Whole Life Insurance

Whole Life Insurance falls under permanent Life Insurance.

As long as premiums remain current, coverage generally lasts throughout life.

Unlike term coverage, whole life includes two components:

Death benefit

Cash value accumulation

Part of each premium contributes toward building cash value over time.

Advantages of Whole Life Insurance

Whole life policies provide:

Lifetime coverage

Coverage generally remains active permanently.

Predictable premiums

Payments often stay fixed.

Cash value growth

Funds accumulate gradually.

Potential borrowing options

Policyholders may borrow against accumulated value.

For individuals focused on long-term planning and wealth transfer, whole life can become part of a larger financial strategy.

Considerations Before Choosing Whole Life Insurance

Whole life policies often come with:

Higher premiums

More complexity

Long-term commitments

While cash value may provide flexibility, buyers should understand fees and policy structure before committing.

Universal Life Insurance

Universal Life Insurance is another permanent policy option with added flexibility.

These policies typically allow adjustments to:

Premium amounts

Death benefits

Payment schedules

This flexibility appeals to individuals with changing financial situations.

Advantages of Universal Life Insurance

Potential benefits include:

Adjustable structure

Policies adapt as needs evolve.

Long-term coverage

Protection can remain in force for life.

Cash value growth opportunities

Depending on policy design.

Greater customization

Useful for evolving financial goals.

Risks to Understand

Flexibility can create complexity.

Poorly managed policies may:

Underperform projections

Require additional premiums

Lose value over time

Understanding policy assumptions is extremely important.

Variable Life Insurance

Variable Life Insurance combines permanent protection with investment options.

Cash value may be invested into market-based subaccounts.

Potential investment choices can include:

Stocks

Bonds

Mutual-fund-style options

Because performance varies with market conditions, growth potential may increase.

However, risk also increases.

Advantages of Variable Life Insurance

Possible benefits:

Investment opportunities

Potential for higher returns.

Tax advantages

Growth may occur tax-deferred.

Flexible wealth planning

May complement broader financial strategies.

Risks of Variable Policies

Investment performance can fluctuate significantly.

Potential concerns:

Market losses

Greater complexity

Higher fees

Unpredictable outcomes

Variable policies generally suit individuals comfortable with investment risk.

Indexed Universal Life Insurance

Indexed Universal Life Insurance (IUL) has gained attention in recent years.

These policies link cash-value growth to market indexes such as:

S&P 500

Other benchmark indexes

Growth typically includes caps and participation limits.

This means policyholders receive partial exposure—not direct market ownership.

Potential Benefits of Indexed Universal Life Insurance

Advantages may include:

Upside growth potential

Without direct market investment.

Downside protection features

Some policies limit losses.

Tax-deferred accumulation

Useful for long-term planning.

Flexible policy structure

Adaptable over time.

Areas Requiring Careful Review

Indexed products often include:

Complex formulas

Participation rates

Caps

Fees

Always request clear illustrations before purchasing.

Final Expense Insurance

Final expense insurance is designed specifically to cover:

Funeral costs

Burial expenses

Medical balances

Smaller debts

Coverage amounts are generally lower than traditional policies.

This option often appeals to older individuals seeking simplified coverage.

Group Life Insurance

Many employers provide Life Insurance through workplace benefit packages.

Benefits may include:

Minimal underwriting

Employer contributions

Convenience

However, group policies often have limitations:

Coverage may end when employment changes

Benefit amounts may be limited

Portability varies

Employer coverage can be valuable—but relying solely on it may create gaps.

How to Choose the Right Type of Life Insurance

Selecting Life Insurance isn't about choosing the "best" policy.

It's about choosing the right policy for your goals.

Ask yourself:

Who depends on me financially?

How long will protection be needed?

What debts need coverage?

Do I want temporary or lifelong protection?

Is cash-value growth important?

What fits my budget?

Different answers create different strategies.

Life Insurance and Legacy Planning

Legacy extends beyond financial inheritance.

Your legacy includes:

Family security

Opportunities for future generations

Financial stability

Values and planning

The right Life Insurance strategy can support:

Children's futures

Charitable giving

Business succession

Estate preservation

Wealth transfer

Protecting your legacy means preparing thoughtfully—not reactively.

Common Mistakes People Make With Life Insurance

Many people delay important decisions because they assume they have time.

Common mistakes include:

Waiting too long

Age and health affect costs.

Buying insufficient coverage

Underestimating needs creates risk.

Choosing solely on price

Cheaper isn't always better.

Ignoring policy details

Fine print matters.

Failing to review coverage

Needs evolve over time.

Regular reviews help ensure protection remains aligned with life changes.

FAQ

1. What type of Life Insurance is best for most families?

Many families begin with term coverage because it provides affordable protection during major financial years.

2. Is Life Insurance only necessary for parents?

No. Single individuals, business owners, and people with debts or dependents may also benefit.

3. Can I have multiple Life Insurance policies?

Yes. Many individuals layer coverage for different goals.

4. Does employer coverage provide enough protection?

Not always. Workplace coverage may be limited and may not transfer when employment changes.

5. When is the best time to buy Life Insurance?

Generally, earlier purchases may provide lower premiums and broader eligibility.

Final Thoughts

Protecting your legacy is not simply about preparing for the unexpected.

It is about creating security, preserving opportunities, and ensuring the people you care about are supported long after you're gone.

The world of Life Insurance can initially seem complex, but understanding the different options transforms uncertainty into confidence.

Whether you choose Term Life Insurance, Whole Life Insurance, Universal Life Insurance, or another strategy entirely, the goal remains the same:

Protect what matters most.

Because your legacy deserves more than hope.

It deserves a plan.