0% Balance Transfer Credit Cards: Are They Worth It?

Introduction: The Promise of Interest-Free Debt Relief

Credit card debt has a way of growing quietly. A few purchases here and there can eventually turn into large balances with high interest rates that feel impossible to escape. For many Americans, the challenge isn't only paying off debt—it's fighting the interest that keeps adding up every month.

That's where 0% balance transfer credit cards enter the conversation.

You've probably seen advertisements promising "0% APR for 12–21 months" and wondered whether it's truly a smart financial move or just another marketing tactic. It sounds almost too good to be true: move your debt to a new card and avoid interest temporarily.

But are 0% balance transfer credit cards actually worth it?

The answer depends on how they're used.

For some people, they can become a powerful tool for paying down debt faster and saving hundreds—or even thousands—of dollars in interest. For others, they can accidentally create more financial problems if used without a plan.

Let's break it down in plain English.

What Is a 0% Balance Transfer Credit Card?

A balance transfer credit card allows you to move debt from one credit card account to another. The main attraction is the introductory 0% Annual Percentage Rate (APR) offered for a limited period.

Instead of paying high interest rates—often between 20% and 30%—you temporarily pay no interest on transferred balances.

For example:

Imagine you owe:

Credit Card Debt: $5,000

Current Interest Rate: 24% APR

Monthly Payment: $150

A large portion of your monthly payment goes toward interest rather than reducing your actual debt.

If you transfer that balance to a card with a 0% introductory APR for 18 months, your payments can focus almost entirely on reducing the principal balance.

That creates breathing room.

And for many people, breathing room matters.

How Balance Transfers Actually Work

The process is fairly straightforward:

Step 1: Apply for a New Card

You apply for a balance transfer card offering an introductory promotion.

Approval often depends on:

Credit score

Debt-to-income ratio

Income

Existing debt obligations

Generally, stronger credit profiles receive the best offers.

Step 2: Request the Transfer

After approval, you submit details about the debt you want moved.

The card issuer usually pays your existing lender directly.

Step 3: Repayment Begins

Your transferred balance appears on your new card, and the promotional period starts.

From this point forward, the clock is ticking.

Major Benefits of a 0% Balance Transfer Credit Card

Balance transfer cards can offer real advantages when used strategically.

1. Significant Interest Savings

This is the biggest reason people use them.

Consider this example:

$7,000 debt at 25% APR can cost thousands in interest over time.

Eliminating interest—even temporarily—can accelerate payoff dramatically.

Instead of your money going toward interest charges, more of each payment attacks the debt itself.

2. Faster Debt Payoff

Without interest constantly increasing your balance, progress becomes visible.

Many people become more motivated when they can actually see debt shrinking month after month.

Financial momentum matters psychologically.

3. Debt Consolidation Simplicity

Some people carry balances across:

Store cards

Travel cards

Retail financing accounts

Multiple credit cards

Combining debt into one payment can simplify budgeting and reduce stress.

Less confusion often leads to better financial decisions.

4. Temporary Financial Relief

Life happens.

Unexpected expenses, emergencies, and income disruptions occur.

A 0% APR period can provide a window to regain financial control without interest adding pressure.

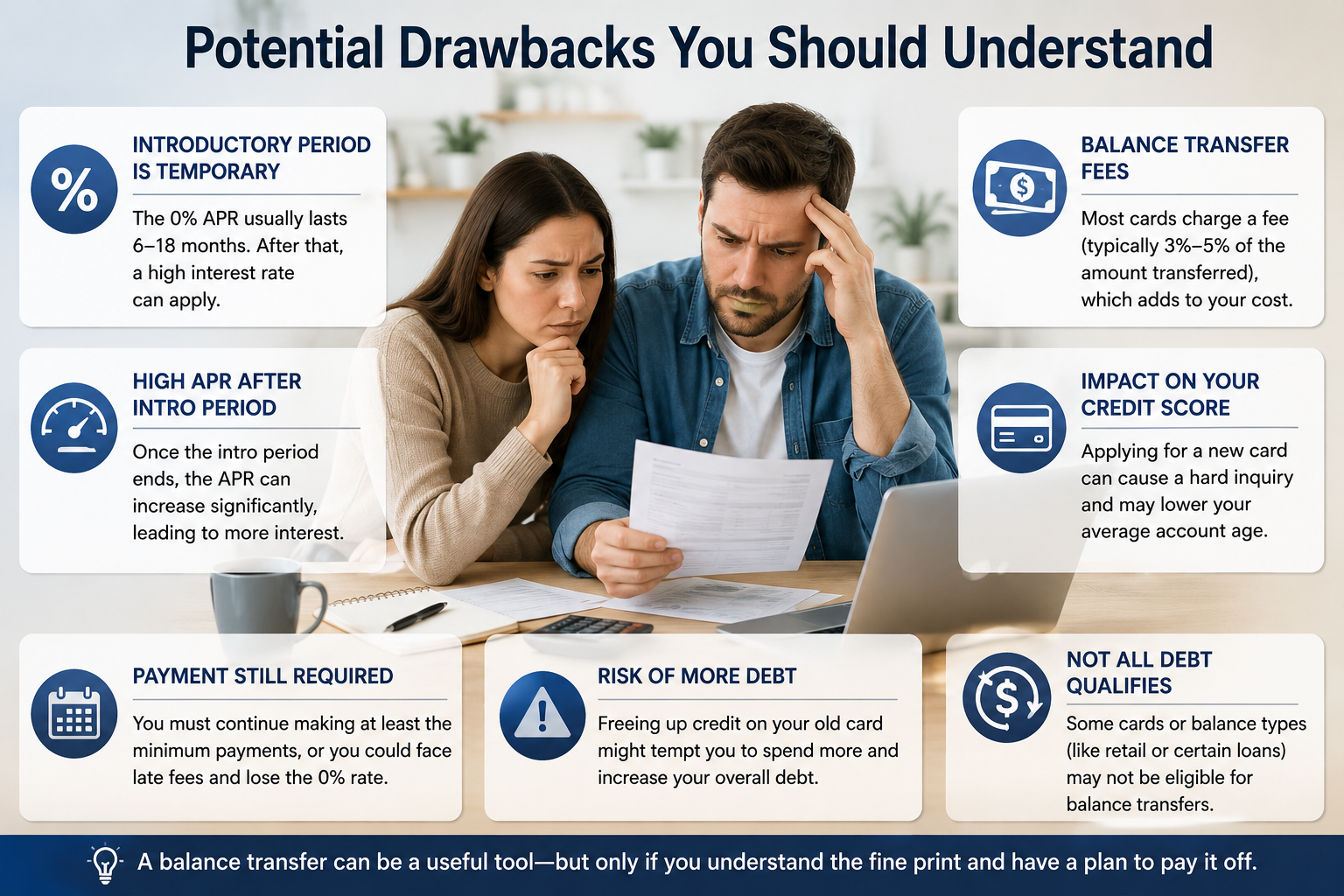

Potential Drawbacks You Should Understand

Balance transfers aren't free money.

There are risks many consumers overlook.

Balance Transfer Fees

Most cards charge transfer fees.

Typical fee:

3%–5% of transferred balances.

Example:

Transfer amount: $8,000

Transfer fee at 5%:

$400

That's a significant upfront cost.

Even with fees, interest savings may still outweigh costs—but always run the numbers.

Promotional Periods End

This is where mistakes happen.

The introductory offer eventually expires.

If you still carry debt afterward, the remaining balance often shifts to a much higher APR.

And that rate can be substantial.

Many people underestimate how quickly promotional periods pass.

New Spending Can Create Problems

A common trap:

People transfer balances, feel financial relief, and begin using old cards again.

Now they have:

New debt on old cards

Existing transferred debt

Additional financial pressure

Without discipline, debt can actually increase.

Approval Isn't Guaranteed

The most attractive offers typically go to consumers with:

Good credit

Very good credit

Excellent credit

Individuals with lower scores may receive:

Smaller credit limits

Shorter promotions

Less favorable terms

Who Benefits Most from Balance Transfer Cards?

Balance transfer cards can work exceptionally well for certain people.

They may make sense if you:

Have a Clear Repayment Plan

The goal isn't simply moving debt.

The goal is eliminating debt.

Before transferring balances, calculate:

Monthly payment needed ÷ promotional months available

If you owe $6,000 with an 18-month offer:

$6,000 ÷ 18

You'd need around $334 monthly.

Simple planning creates better outcomes.

Have Stable Income

Consistency matters.

Reliable income improves your ability to eliminate balances before promotional periods expire.

Can Avoid New Debt

Balance transfers work best when spending habits improve alongside financial strategy.

The card creates opportunity.

Behavior creates results.

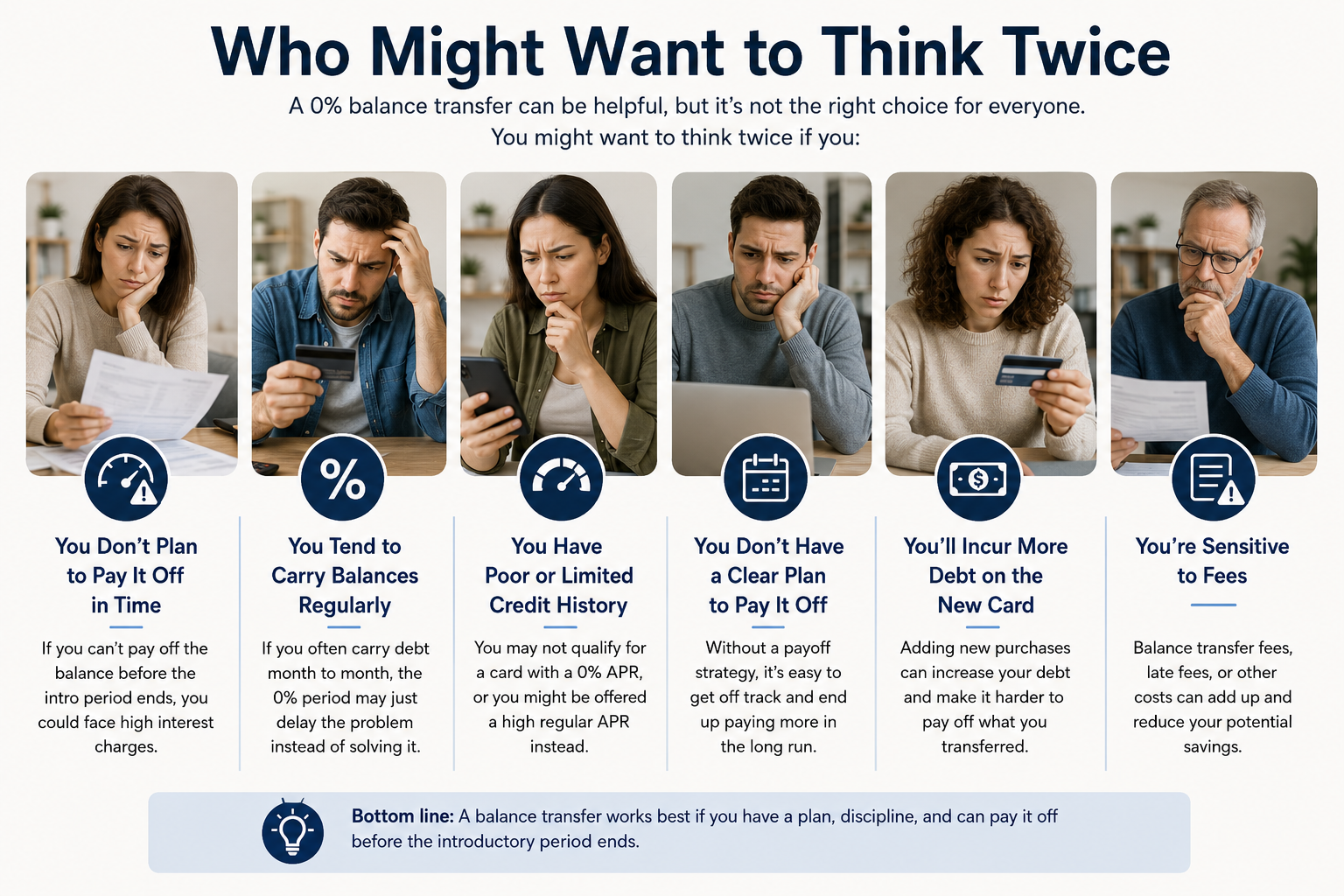

Who Might Want to Think Twice?

Balance transfers may not be ideal if:

Your debt continues increasing monthly

Your budget remains unstable

You struggle with impulse spending

You can only afford minimum payments

Your credit profile is weak

In these situations, other approaches may deserve consideration.

Examples include:

Debt management plans

Personal loans

Credit counseling

Budget restructuring

Financial tools work differently for different situations.

Common Myths About Balance Transfer Cards

Myth: They're Completely Free

Reality:

Fees often exist.

Read terms carefully.

Myth: They Erase Debt

Reality:

Debt doesn't disappear.

It simply moves.

You still owe the same principal amount.

Myth: Everyone Qualifies

Reality:

Approval standards vary considerably.

Credit quality matters.

Myth: One Transfer Solves Everything

Reality:

Long-term financial habits determine outcomes.

The card itself isn't the solution.

Your behavior is.

Questions to Ask Before Applying

Before submitting an application, ask:

How much debt am I transferring?

What is the transfer fee?

How long does the 0% period last?

Can I realistically pay this off in time?

Will I avoid accumulating additional debt?

These questions can prevent expensive mistakes.

Final Verdict: Are 0% Balance Transfer Credit Cards Worth It?

For many people, yes.

When used responsibly, a 0% balance transfer credit card can become a valuable financial strategy that saves money, reduces interest costs, and accelerates debt payoff.

But success isn't automatic.

The best outcomes happen when consumers:

Understand fees

Create a repayment plan

Avoid new spending

Commit to long-term financial improvement

Balance transfer cards aren't magic solutions.

They're tools.

And like any financial tool, results depend on how you use them.

Ready to Take the Next Step?

Ready to go deeper? Explore resources from Ascendia Legacy Group, including guides like 700+ Blueprint and other financial tools designed to help you build a stronger future.

Because financial knowledge isn't just about managing debt—it’s about creating opportunities for the future.