15 Questions to Ask Lenders Before Committing to a Personal Loan

Taking out a personal loan can be a practical solution when you need funds for debt consolidation, emergency expenses, home improvements, medical bills, or major purchases. But signing a loan agreement without asking the right questions can lead to costly surprises down the road.

Many borrowers focus only on the monthly payment and interest rate. However, hidden fees, loan terms, repayment flexibility, and lender policies can significantly affect the total cost of borrowing.

Before committing, take time to understand exactly what you're agreeing to. Asking the right questions helps you avoid financial mistakes and ensures the loan truly fits your needs.

Here are 15 important questions to ask lenders before committing to a personal loan.

1. What Is the Interest Rate?

Interest rate is one of the first things borrowers ask about—and for good reason.

Even a small difference in percentage points can dramatically affect how much you pay over time.

Ask:

Is the rate fixed or variable?

Is this the lowest possible rate?

Does my credit score affect eligibility?

A fixed rate stays the same throughout the loan term, while a variable rate can change over time.

Don't focus solely on monthly payments; understand how the interest impacts total repayment.

2. What Is the APR?

Many borrowers confuse interest rates with APR (Annual Percentage Rate).

APR includes:

Interest charges

Origination fees

Certain lender costs

APR often provides a more accurate picture of the true cost of borrowing.

A loan with a lower interest rate but higher fees may actually cost more overall.

Always compare APRs when shopping among lenders.

3. Are There Origination Fees?

Some lenders charge an origination fee for processing the loan.

These fees commonly range from:

1%–8% of the loan amount

Example:

If you borrow $10,000 and pay a 5% origination fee, you may only receive $9,500 while still repaying the full amount.

Always ask:

"Will any fees be deducted before I receive my funds?"

4. Are There Prepayment Penalties?

Paying off debt early sounds responsible—but some lenders penalize borrowers for it.

Ask whether you can:

Pay extra each month

Make larger principal payments

Pay the loan off entirely early

The best personal loans typically allow early repayment without penalties.

Flexibility matters.

5. What Will My Monthly Payment Be?

Understanding the exact monthly payment prevents surprises.

Request details including:

Payment amount

Due date

Loan duration

Total repayment amount

Even affordable monthly payments can become expensive if the repayment period stretches too long.

6. How Long Is the Loan Term?

Loan terms commonly range from:

12 months

24 months

36 months

60 months

Longer

Longer terms reduce monthly payments but often increase overall borrowing costs.

Ask lenders to show multiple repayment scenarios.

7. What Is the Total Cost of the Loan?

This is one of the most overlooked questions.

Ask:

"How much will I pay from start to finish?"

This includes:

Principal

Interest

Fees

Added charges

Knowing the total cost gives a realistic understanding of your financial commitment.

8. Is My Credit Score Going to Affect Approval?

Personal loan requirements vary significantly.

Some lenders specialize in:

Excellent credit

Fair credit

Bad credit

Debt consolidation borrowers

Ask:

Minimum score requirements

Factors considered beyond scores

Whether prequalification is available

Prequalification often allows you to estimate terms without damaging your credit.

9. Does Applying Affect My Credit Score?

Some lenders use:

Soft inquiries

These usually don't impact credit scores.

Hard inquiries

These can temporarily lower scores.

Before applying, ask how credit checks are handled.

10. Are There Late Payment Fees?

Life happens.

Unexpected expenses can sometimes make repayment difficult.

Ask:

Late payment fee amounts

Grace periods

Reporting policies

Missing payments can affect both your finances and your credit report.

11. What Happens If I Miss Payments?

Understanding lender hardship policies is critical.

Ask if they offer:

Payment extensions

Temporary hardship programs

Modified repayment plans

Knowing your options before financial problems occur creates peace of mind.

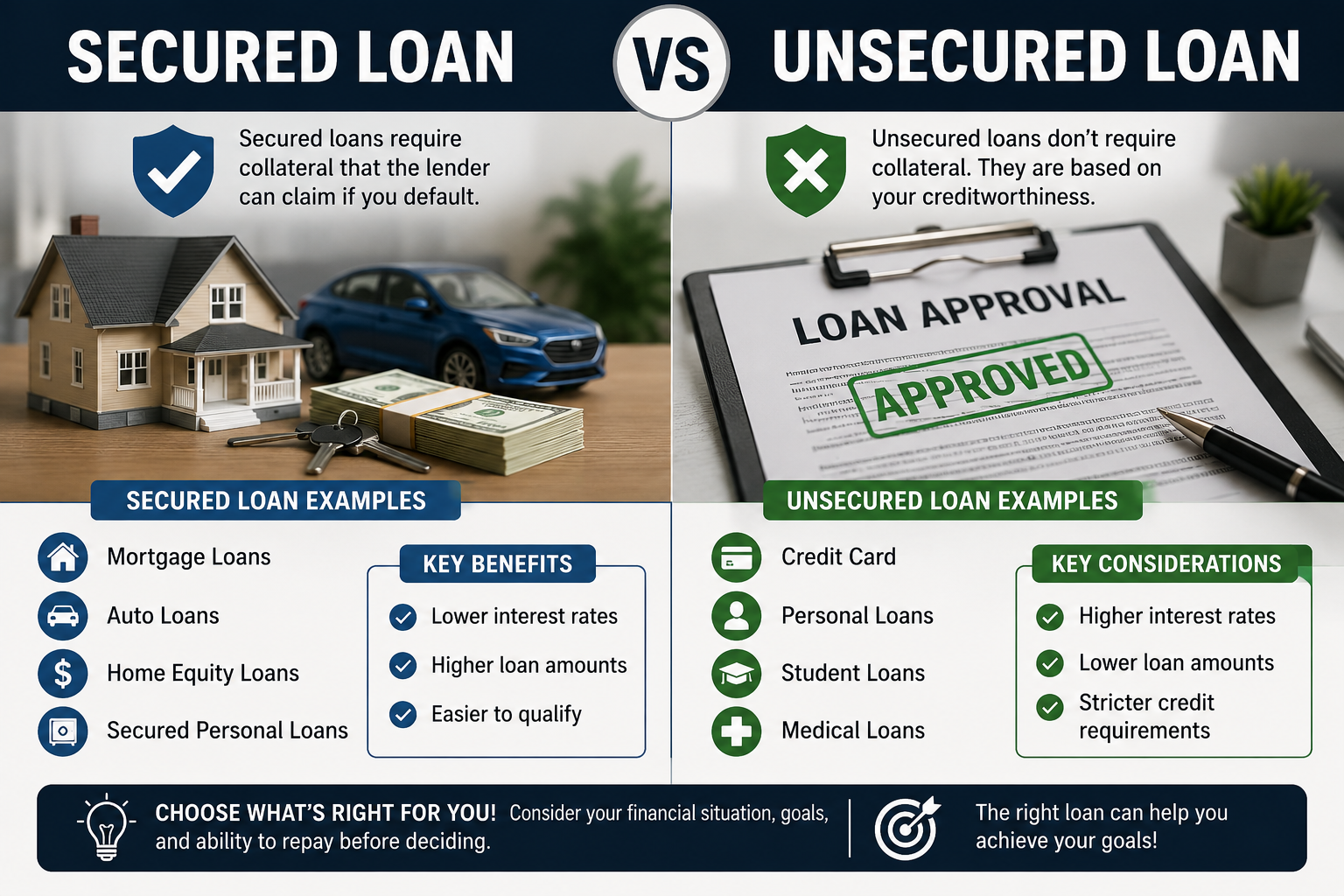

12. Is the Loan Secured or Unsecured?

Personal loans generally fall into two categories:

Secured loans

Require collateral such as:

Vehicles

Savings accounts

Assets

Unsecured loans

Require no collateral but may carry higher rates.

Always understand what you're risking.

13. Can Loan Terms Change After Approval?

Some borrowers assume pre-approved offers are guaranteed.

Ask whether:

Terms can change during underwriting

Rates may increase

Conditions can be added

Read final agreements carefully before signing.

14. How Quickly Will I Receive Funds?

Timing matters when borrowing.

Funding times vary:

Same day

24–48 hours

Several business days

Emergency borrowers especially should verify timelines beforehand.

15. Is There Anything in the Fine Print I Should Know?

This question often reveals unexpected details.

Ask lenders directly:

"Are there any conditions borrowers frequently overlook?"

Watch for:

Administrative fees

Auto-payment requirements

Insurance add-ons

Cancellation policies

Never rush through loan documents.

Fine print matters.

Red Flags to Watch Out For

Beyond asking questions, watch for warning signs:

Pressure to decide immediately

Vague fee explanations

Guaranteed approvals

Extremely high rates

Requests for upfront payment

Poor customer reviews

Trustworthy lenders should answer questions clearly and transparently.

FAQ

1. How many lenders should I compare before choosing a personal loan?

Compare at least three to five lenders. Multiple offers help identify better rates and terms.

2. Can I negotiate personal loan terms?

Sometimes. Borrowers with stronger credit profiles may receive flexibility on rates and fees.

3. Is online prequalification safe?

Yes, reputable lenders commonly offer secure prequalification processes.

4. Should I take the lowest monthly payment?

Not necessarily. Lower monthly payments often increase total repayment costs.

5. What's more important: APR or interest rate?

APR usually provides a clearer picture because it includes fees and additional costs.

Final Thoughts

A personal loan can help solve financial challenges—but only if you understand what you're signing up for. Asking smart questions before committing protects you from hidden costs and future stress.

The best borrowers are informed borrowers.

Before agreeing to any loan, slow down, compare options, and ask these 15 questions. A few minutes of research today can save thousands of dollars tomorrow.